Sunday Review + Watchlist 3/8/26

Geopolitical Driven Market

(Trying a new approach to this Sunday’s Review - let me know what you think)

Market Recap

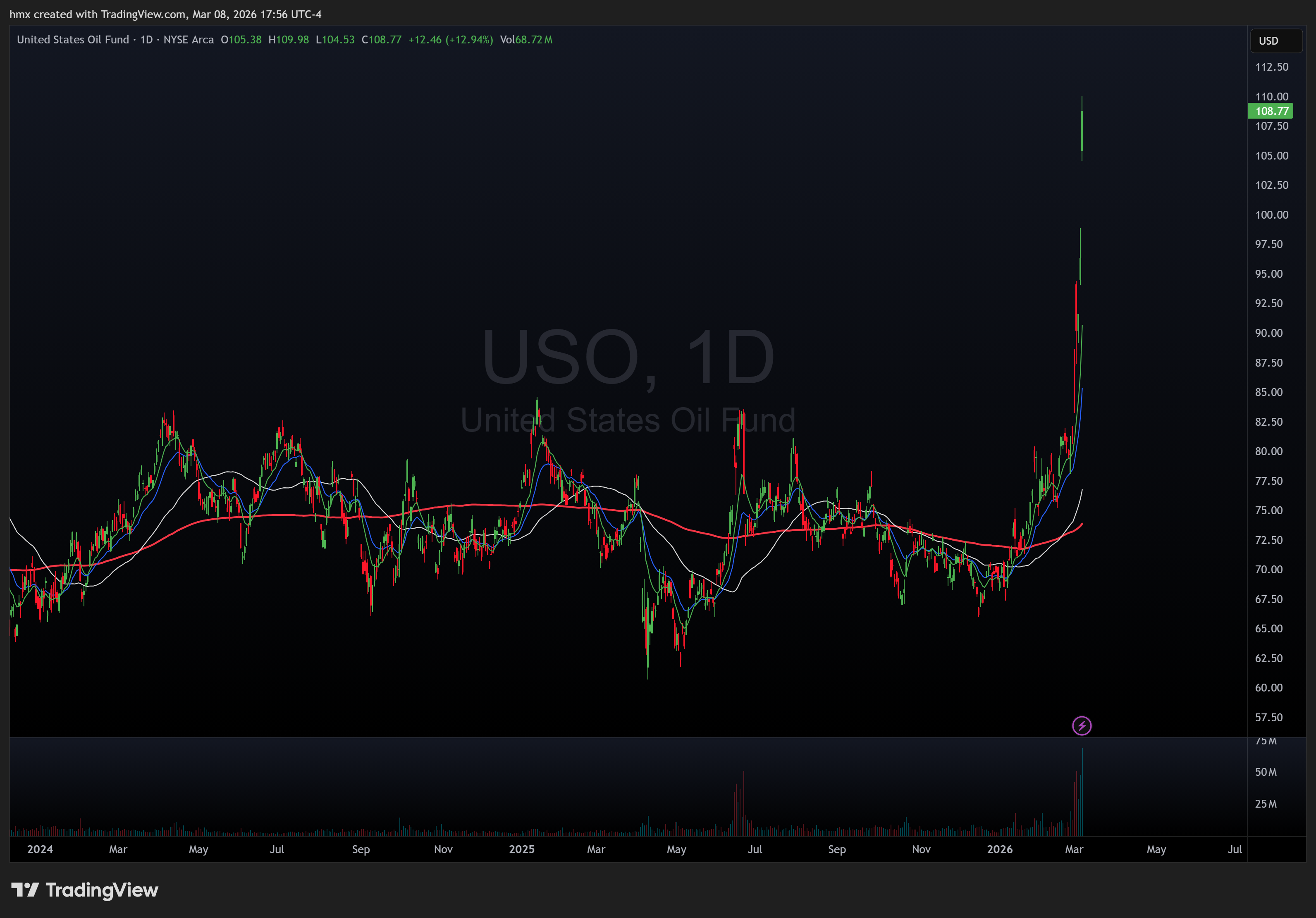

This was a war week, and everything else was background noise. US and Israel launched strikes on Iran starting last Saturday, Iran retaliated across the Gulf, and within days the Strait of Hormuz went from the world’s most important oil chokepoint to a no-go zone. Zero crude or LNG transits on Sunday and Monday. Fifty-five fully loaded supertankers sat stranded in the Gulf by midweek. Kuwait declared force majeure. Saudi Arabia’s Ras Tanura refinery got hit by drones and went offline. Qatar shut down LNG production. WTI 0.00%↑ ripped past $90 on Thursday for the first time since October 2023, up roughly 25% in four sessions, on track for the largest weekly percentage gain in at least two decades.

Citigroup estimated 7 to 11 million barrels per day temporarily removed from global supply. That’s not just a headline, that’s a regime change for energy markets. XOM 0.00%↑ and CVX 0.00%↑ were obvious beneficiaries, with CVX showing relative strength on Friday while nearly everything else bled.

Tanker names like FRO 0.00%↑ and oil services like SLB 0.00%↑ pulled back all week. On the other side of that trade, airlines got destroyed with UAL 0.00%↑ and ALK 0.00%↑ both down over 3% on Friday alone.

The S&P 500 SPY 0.00%↑ dropped about 1.3% on Friday alone to close at 6,740, and the breadth numbers told the real story: 59% of components were sitting at five-day new lows while only 8% made new highs. The Nasdaq QQQ 0.00%↑ fell 1.5% Friday and gave back everything from Wednesday’s bounce. The week had a choppy rhythm to it. Monday gapped down hard on the Iran news, Wednesday rallied on a brief “economic resilience” narrative, and then Thursday and Friday sold off as oil kept screaming higher and the February jobs report came in at negative 92,000 versus expectations of positive 59K.

Defense names soaked up the fear bid, with PLTR 0.00%↑ spiking nearly 6% intraday Monday on the classic war rotation, though it’s still down 18% year to date and just confirmed a death cross. CRWD 0.00%↑ beat earnings by a mile, 51% EPS beat, and barely got a sustained reaction because nobody cared about cybersecurity margins when crude is repricing the entire market. Meanwhile NVDA 0.00%↑ dropped a $2 billion investment into COHR 0.00%↑ for AI optical networking, sending it up 10% Monday, but even that got swallowed by the broader risk-off.

Crypto, semis, and high-beta growth all got hit. ASML 0.00%↑ down 5.5%, MSTR 0.00%↑ down 4.5%, Bitcoin IBIT 0.00%↑ back to $67K.

Heading into next week, there’s really only one question: does the Hormuz disruption persist or start to de-escalate? Israel struck Tehran fuel storage terminals on Saturday and Trump promised to hit Iran “very hard” again, so the answer right now leans toward escalation. If crude holds above $90, expect continued rotation into energy and defense while growth and anything rate-sensitive stays under pressure.

Low-Float Small Caps

MOBX 0.00%↑ was a top gainer this week, ripping over 500% from $0.17 to a high of $1.33 on absolutely absurd volume, turning over nearly 2.5 billion shares against an 83.7 million share float. While it closed the week near $1.04, the move from sub-$0.20 was the kind of parabolic action that defines these cycles. BATL 0.00%↑ also had a monster week, doubling off $10.70 and tagging nearly $30 before settling around $22.36, showing more staying power than most low-float runners tend to. PRSO 0.00%↑ ran 145% and actually held near highs, closing at $2.04 just under its $2.10 weekly peak. TPET 0.00%↑ was another name that caught a bid, gaining 83% on 1.5 billion shares traded, though it gave back a decent chunk from its $2.50 high to close at $1.93.

On the other side, several names this week were textbook supply plays. CANF 0.00%↑ is the poster child, ripping from $4.51 all the way to $10.40 intraday before round-tripping the entire move and closing at $4.55, basically unchanged on the week. TMDE 0.00%↑ ran a similar script, pushing to $4.77 before fading back to $2.92. GXAI 0.00%↑ gained 52% on the week but gave back significantly from its $2.43 high. INDO 0.00%↑ and HYMC 0.00%↑ were the clean backside fades, dropping 33% and 22% respectively as prior momentum unwound.

Watchlist

USO 0.00%↑ - huge move in oil last week and starting to look extended, but momentum can carry this higher so it’s the main watch heading into Monday.

IBIT 0.00%↑ - bitcoin and crypto names tried to break out of their short term bases but quickly fell back into range, signaling weakness and no follow through.

BATL 0.00%↑ / TPET 0.00%↑ - small cap oil names riding the crude move, watching for an open bias play if they gap with volume.

VXX 0.00%↑ - headline prone market with the Iran situation still unfolding, expect another volatile week and vol names stay in play.

Upcoming Economic Events and Earnings

Tuesday 3/10 AH | ORCL Earnings | Impact: MED | stock is down 50% since Sept, big reaction either way could ripple through cloud/AI names

Wednesday 3/11 8:30 AM | February CPI | Impact: HIGH | the single biggest print of the week — expect wide spreads and whippy price action all morning, size accordingly

Thursday 3/12 8:30 AM | PPI | Impact: MED | day after CPI so market already has inflation context, but a surprise here can reignite vol heading into Friday’s PCE

Thursday 3/12 AH | ADBE Earnings | Impact: HIGH | sets tone for Friday open in tech/growth, elevated vol in software names

Friday 3/13 8:30 AM | Core PCE + Q4 GDP (2nd est) + UMich Sentiment | Impact: HIGH | triple data dump at open — PCE is the Fed’s preferred inflation gauge, GDP revision, and first sentiment read since the Iran conflict started. Messy open guaranteed.

Geopolitical overlay all week: the US-Iran conflict is the wildcard that overrides everything. Energy names especially volatile, and any headline can blow up a clean setup mid-session.

Happy trading!