The Concept That Quietly Changed My Trading

How Math Makes It Impossible To Lose In Trading

For a long time, I thought trading was about being right. More green days than red days. More winners than losers. That’s what I focused on in the early days, and honestly, that’s what most people focus on when they start. And for a while, it felt like it was working.

I had weeks where I won a lot of trades, felt confident, and felt like things were finally clicking. But when I stepped back and looked at my account over a longer stretch of time, the results didn’t line up with how “good” I felt about my trading.

That disconnect was my first real wake-up call.

The Problem With How Most Traders Measure Success

Early on, I tracked everything in dollars. Green day or red day. That was it. The problem is that dollars don’t tell you anything about quality. They don’t tell you how much you risked to make what you made, or whether a win was the result of a solid process or just luck.

I could have a $500 green day that came from oversized risk and poor discipline, and a $200 red day that was actually a well-executed trade that simply didn’t work.

Emotionally, the green day felt like success and the red day felt like failure, even though the opposite was often true. That way of thinking kept me stuck longer than it should have.

It all comes down to this:

It’s not your win rate that matters. It’s the relationship between your win rate and your average R-multiple.

Discovering R-Multiples

Everything began to change when I started measuring trades in R-multiples.

R stands for Risk. One R is the dollar amount I am willing to lose on a trade if I am wrong. That amount is defined BEFORE I enter, based on where my stop is. Once I started doing that, every outcome had context.

My R-multiple is how much I make or lose relative to that fixed risk.

If I risk $200 on a trade and make $200, that’s +1R

If I risk $200 and make $600, that’s +3R

If I lose the $200, that’s -1R

This immediately exposed something uncomfortable. A lot of my “winning” trades were actually small R wins, while my losing trades were often larger than -1R because I was slow to stop out or emotionally attached. On paper, I was winning. In reality, my math was broken.

There are a few ways to define your R, but the simplest way I’ve found is to use a percentage of your account, which I’ll talk about more below.

Why Win Rate Alone Is a Trap

This is where most traders get fooled. You can win a high percentage of your trades and still lose money if your losers are larger than your winners. I lived this. There were stretches where I felt great because I was right more often than not, but when I looked at my R data, it told a very different story. Eight small wins and two large losses can easily cancel each other out, sometimes worse. I was bleeding slowly without even realizing it:

Example A:

8 wins × +0.5R = +4R

2 losses × -2R = -4R

Net = 0R

That’s breakeven at best, and it doesn’t even factor in slippage, commission, and ECN fees.

Example B:

3 wins × +3R = +9R

7 losses × -1R = -7R

Net = +2R

Lower win rate, higher profitability.

Once I started focusing on R, I realized I didn’t need to be right all that often. I just needed my winners to be meaningfully larger than my losers. That realization completely changed how I approached trades and how patient I was willing to be when something was actually working.

There Is A Limit to Win Rate

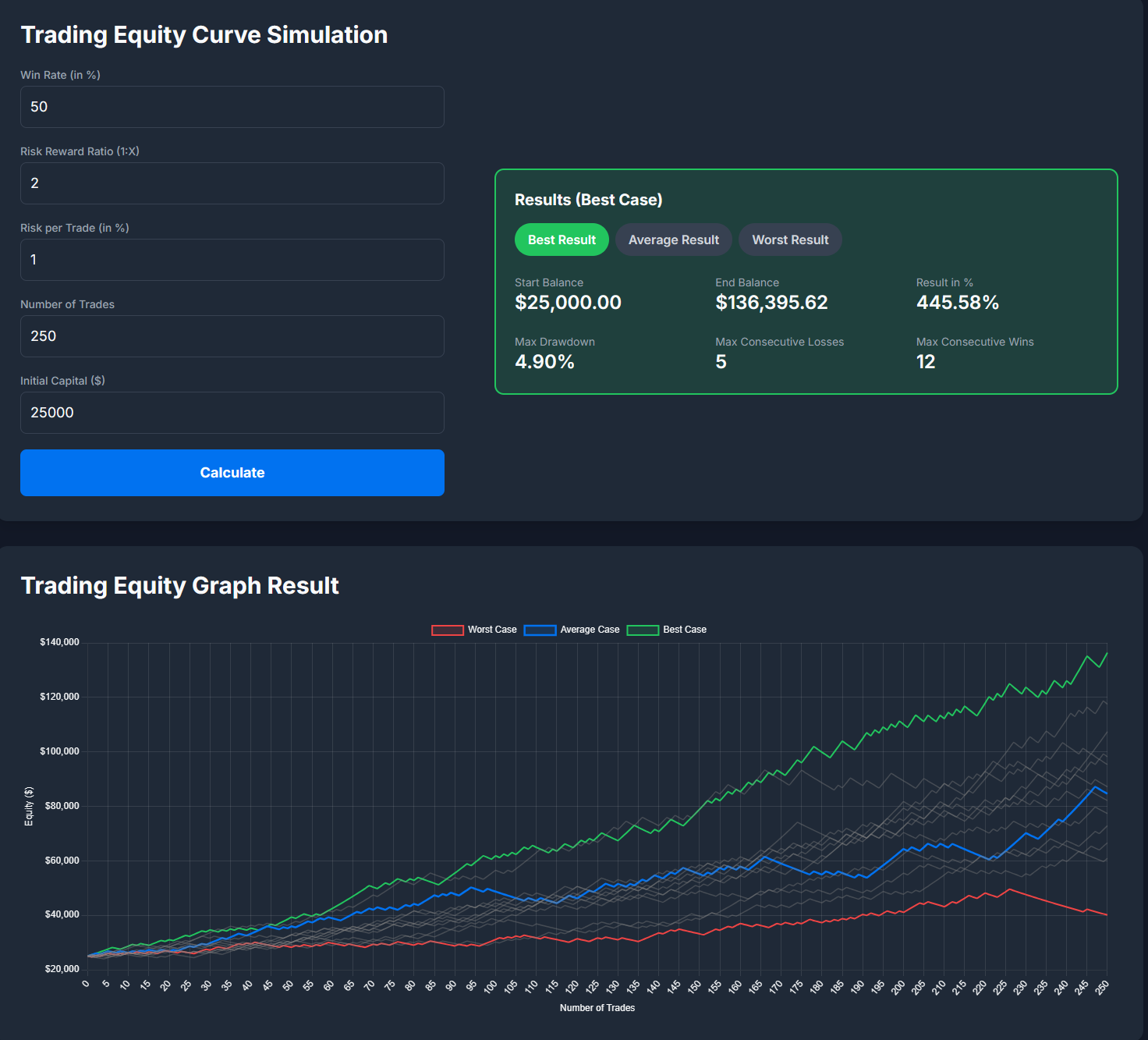

I wanted to know the limits of my systems and see how low of a win rate was acceptable while still staying profitable. I found with a 2:1 RR (risk to reward ratio), meaning my average win is 2x my average loss, I only need to win a little over 33% of the time to be better than breakeven.

Having a 2:1 RR with a 50% win rate is a very profitable system (simulated below). You can see from the chart how linear the equity curve is with only a max drawdown of 4.90% which is very stable. You get a return of over 400% on a 25k account.

Think about this - if you can get your average RR to 3:1 (which is very reasonable), it would be extremely difficult to not make money since you would need to be wrong more than 75% of the time!

Enter Position Sizing: The Hidden Driver

R-multiples only matter if your risk is consistent and that’s where position sizing comes in. You can have the best edge in the world, but if your position size is inconsistent, or worse, emotional, your results will be too.

When I first started, I sized trades based on confidence. If I liked something more, I took more size. If I felt unsure, I took less (that’s called exponential bet sizing and it can work, but it’s an advanced technique that I wont cover here). It felt logical at the time, but it introduced massive inconsistency and made it almost impossible to evaluate whether my edge actually worked.

Once I committed to risking a fixed percentage of my account per trade, everything stabilized. Every trade starts with a thesis, and that thesis has a clear point where it is wrong. That invalidation level is what defines risk.

Here’s how it works:

If my account was $25,000 and I risked 1% per trade, that meant every trade carried the same $250 risk. The position size changed based on the stop, not my emotions.

If my stop is $0.50/share, I buy 500 shares.

If my stop is $1.00/share, I buy 250 shares.

For example, say I want to buy AAPL at 260 because it’s breaking out on the daily chart. My thesis is that the breakout should hold. If price breaks back below 255, that thesis is invalid. That means my stop is five dollars away. If I want to risk $250 on the trade, I simply divide the dollar risk by the stop distance. Five dollars of risk means I can buy 50 shares. I let math drive my system, not emotion.

This approach keeps everything consistent. A trade with a wide stop naturally gets smaller size. A trade with a tight stop gets larger size. In both cases, the risk stays the same. Once I committed to risking a fixed percentage of my account per trade, my results stabilized and my decision-making became much cleaner. Losing streaks became survivable, and winning trades actually mattered because they were built on a consistent foundation.

Build a Positive Expectancy System

Once I had enough data by tracking trades in R, the picture became very clear. Trading is not about individual outcomes, it’s about what happens when you repeat the same process over and over again.

Expectancy is simply the relationship between win rate and how much you make and lose. It ties it all together. Here’s the formula:

Expectancy = (Win rate × Avg win R) − (Loss rate × Avg loss R)

Let’s break it down:

Win rate: 40%

Avg win: +2.5R

Loss rate: 60%

Avg loss: -1R

Expectancy = (0.4 × 2.5) − (0.6 × 1) = 1.0 − 0.6 = +0.4R per trade

Now multiply that across 100 trades:

+0.4R × 100 = +40R

If you’re risking $250 per trade, that’s $10,000 in profit on a 40% win rate. And none of that requires a high win rate or perfect execution. It just requires a system with positive expectancy and the discipline to stick to it.

Once I internalized this, it changed how I viewed losing trades. Losses stopped feeling like failure and started feeling like part of the cost of doing business. As long as I was controlling risk and letting winners work, the math would take care of the rest.

What I Pay Attention to Now

I care far less about being right than I used to

I care about defining risk before entry

Keeping losses at -1R

Letting winners work instead of cutting them short, and

Tracking everything in R rather than dollars

When I review my trading now, I’m not asking whether I made money that day. I’m asking whether I executed well relative to my risk. The money takes care of itself if the process is solid.

Final Thought

R-multiples tell you the quality of your trades. Position sizing determines whether that quality shows up in your account. Ignore either, and you’re just guessing.

Most traders don’t fail because they lack setups. They fail because they don’t understand risk and don’t measure their performance correctly. R-multiples changed the way I see trading. They removed a lot of emotion, exposed my real weaknesses, and gave me a framework I could actually build on. Winning trades feel good, but well-structured risk is what lasts.

That’s how you treat trading like a business and compound your edge.

This is great! Thank you.